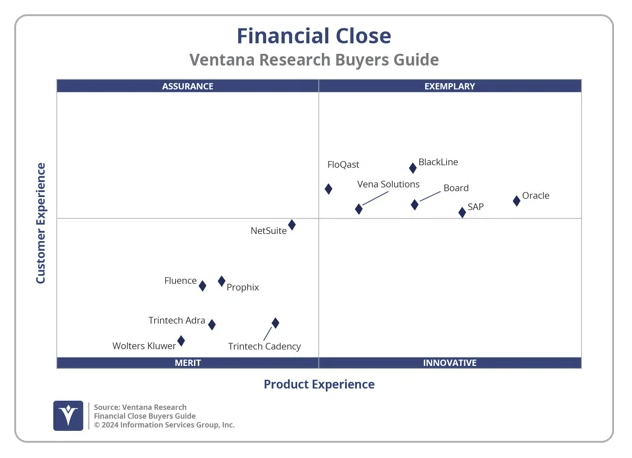

Ventana Research, now ISG Software Research, recently released its 2024 Financial Close Buyers Guide, which ranked BlackLine an Exemplary Vendor and Overall Leader. The report highlighted the total cost of ownership (TCO) and return on investment (ROI) that BlackLine delivers to its customers.

“As the financial landscape continues to evolve, the need for the Office of the CFO to drive business forward has never been more critical,” said Robert Kugel, executive director and head of business research, ISG Software Research. “Blackline’s proven, collaborative and achievable approach to digital transformation has positioned the company as a trusted partner for organizations worldwide.”

The guide evaluated 12 vendors in the financial close software market. They are: BlackLine, Board International, FloQast, Fluence, NetSuite, Oracle, Prophix, SAP, Trintech Adra, Trintech Cadency, Vena Solutions and Wolters Kluwer.

The report uses the Ventana Value Index methodology, which is based on extensive market and product research and is structured to replicate an RFI process by incorporating criteria to select technology. The research evaluates technology providers on products that address critical elements of enterprise software across ten product and customer experience categories.

Ventana ranked BlackLine as a leader in seven out of the ten categories, including Capability, Usability, TCO/ROI and Validation. The company received an overall grade of A-, and was recognized for:

- Product Experience for its manageability, administration, privacy and security.

- Customer experience for its total cost of ownership (TCO) and return on investment (ROI), due to effective systems and processes for managing and escalating breaches.

Vendors in the Exemplary category represent those that performed the best in meeting the overall product and customer experience requirements.

Read the full 2024 Financial Close Management Buyers Guide.

ISG Software Research provides authoritative market research and coverage of the business and IT software industry.